Why Canada’s Internet Costs Are So High (2025 Report)

October 11, 2025

Canadians pay some of the highest Internet prices in the world, and while the reasons are complex, they aren’t mysterious. From wholesale access fees to market consolidation and clever pricing tactics, the system has been structured to reward scale rather than competition. Here’s a data-driven look at what’s really driving those high monthly bills, and how smaller providers are trying to change it.

The Big Picture: High Prices, Limited Competition

Canada consistently ranks among the five most expensive countries for broadband in the developed world, according to OECD broadband statistics.

The CRTC’s 2024 Communications Monitoring Report found that average monthly Internet bills have increased by nearly 8% in just two years, even as the cost of delivering service through shared infrastructure has remained relatively flat.

When introductory promotions, AutoPay discounts, and bundled credits expire, this increase translates into typical real-world monthly Internet bills of roughly $85 to $110 for many Canadian households – a level that is often double what comparable high-speed service costs in other developed countries.

Why Prices Stay High (Even When Costs Don’t)

1. Structural Advantage for Large Carriers

Canada’s telecom market is dominated by a few large players, primarily Bell, Rogers, Telus, and in Quebec, Videotron (Quebecor). These companies own the physical fiber and coaxial networks that most Canadians depend on. Smaller ISPs lease access through CRTC-regulated wholesale agreements.

Those wholesale rates, while designed to ensure competition, still heavily favor incumbents. Large carriers control the upgrade cycle, the infrastructure, and much of the retail market — allowing them to maintain pricing power even as technology improves.

As one telecom analyst told The Globe and Mail, “Canada’s broadband market is structured to reward scale, not competition.”

2. “Profit Efficiency” Tactics

In recent years, major carriers have introduced new ways to quietly increase margins.

Some now require AutoPay enrollment to access their lowest advertised rates. AutoPay can save providers up to 2% in processing fees, yet those savings are rarely passed on to consumers.

At the same time, the industry has seen a steady wave of acquisitions, large telcos buying smaller independents. Each deal adds subscriber volume and revenue, while reducing consumer choice. Recent examples include Bell’s acquisition of Distributel (Primus) and Telus’ purchase of Start.ca.

3. Lack of Effective Market Pressure

With fewer true independents left, the remaining ISPs face high wholesale costs and limited flexibility to lower prices further. The result: a market that appears competitive but behaves like an oligopoly.

Why New Entrants Won’t Fix It Anytime Soon

Every few years, talk resurfaces about a major new carrier entering Canada to “shake up” the telecom market, often an American company rumored to be eyeing expansion north of the border. The reality is far less exciting.

Building a nationwide network from scratch would cost billions of dollars and take years, if not decades. To compete with incumbents, a new provider would need to physically connect millions of homes, which means securing municipal permits, digging up streets to lay fiber or coaxial cable, and deploying thousands of access nodes. The financial barrier is enormous, and Canada’s population density makes it even harder to justify the investment outside major cities.

As a result, most newcomers either lease capacity from existing carriers (becoming resellers rather than true competitors) or look to bypass the ground entirely like Starlink, the satellite Internet service operated by SpaceX. While Starlink has opened access for rural and remote communities, satellite connections come with high latency, bandwidth constraints, and weather interference, making them less practical for urban customers or for mobile/voice service at scale.

Until someone is willing and able to fund a fully independent national network, Canada’s broadband market will continue to rely on the same physical infrastructure controlled by a few dominant players.

“Any new entrant would face the same hard reality,” says one industry analyst. “You can’t disrupt a market when you still depend on your competitors’ networks.”

The Real Cost of Delivering Internet in Canada

Even without the marketing and billing layers, Internet delivery isn’t cheap. Much of your monthly bill goes toward network access fees, regulatory costs, and infrastructure maintenance.

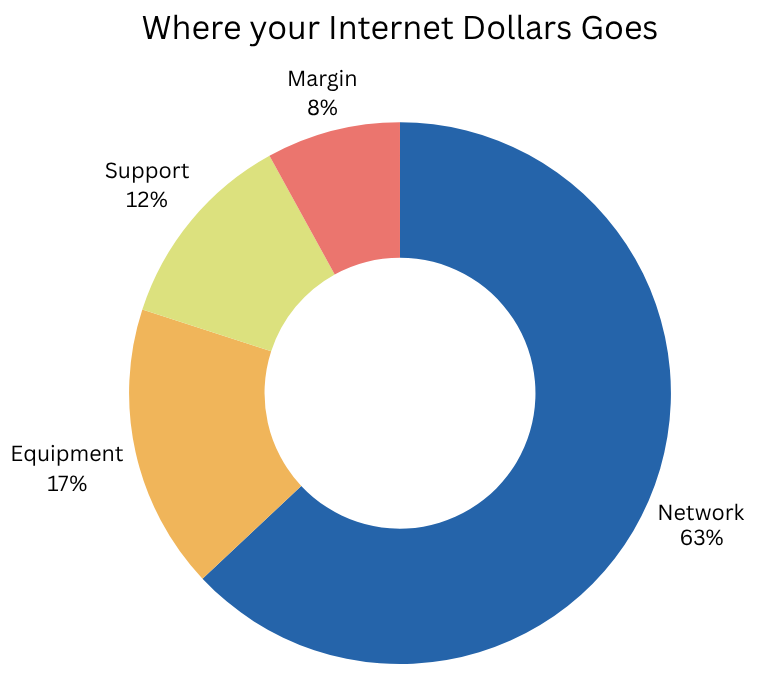

Where Your Internet Dollar Goes (average for smaller ISPs)

Category

Approximate Share

Wholesale Network Access (leased lines)

60–65%

Equipment, Shipping & Setup

15–20%

Customer Support & Operations

10–15%

Margin (sustainability & reinvestment)

5–10%

Smaller ISPs like NetJOI often pay wholesale access fees that consume well over half of every dollar a customer spends before factoring in support or equipment. That’s why independent providers can’t simply undercut big-carrier pricing by 50%, but can offer fairer long-term value through transparent pricing and better service.

To put that into perspective, here’s how a typical Canadian Internet dollar is distributed when you subscribe through a smaller ISP:

Roughly 63% of every payment goes to wholesale access fees, the cost of leasing network infrastructure from national carriers like Bell or Rogers. About 17% covers equipment such as modems and shipping, 12% supports customer care and technical operations, and only around 8% remains as margin.

It’s a structure that explains why independents fight hard to deliver fair pricing as there simply isn’t much room for markups once the wholesale costs are paid.

The Human Cost of Connectivity

For many Canadians, Internet access isn’t optional. It’s a lifeline for work, education, healthcare, and staying connected.

Yet as prices rise faster than wages, broadband affordability is becoming a national issue. In rural and Atlantic regions especially, limited infrastructure and fewer provider choices mean customers pay more for slower speeds.

And while the federal government’s Connecting Canadians initiative aims for universal broadband by 2030, coverage gaps remain especially outside major cities.

How Smaller Providers Help Balance the Market

Independent ISPs bring flexibility and fairness to the table. Without massive marketing budgets or layers of bureaucracy, they compete through transparency, digital-first support, and customer care.

Because they use existing backbone networks, their efficiency comes from operations, not corner-cutting.

For example, in Nova Scotia, many families can access fair-priced, stable Internet from independent providers. And in Ontario, NetJOI’s JOI 75 plan is $59.95/month with locked-in pricing, no contracts, and no sudden rate changes.

Compare the real cost — look at regular (post-promo) rates, not first-year discounts.

Avoid long-term contracts when possible. Flexibility matters more than small short-term savings.

Support independent ISPs that focus on service and stability. Even a modest shift in market share can improve competition.

Question AutoPay requirements and other fine print that affect billing flexibility.

If you’d like to help push for fairer wholesale pricing in Canada, you can also read our Telecom Advocacy Report and sign the petition calling for stronger competition and consumer protection.

Independent ISPs like NetJOI offer a clearer, more predictable alternative with locked-in pricing and digital-first support.

Frequently Asked Questions

Why is Internet so expensive in Canada? Canada’s Internet market is controlled by a few large companies that own both the retail brands and the physical network infrastructure. Smaller ISPs must lease access through regulated wholesale agreements, which keeps costs high and limits true price competition.

Is Canadian Internet getting cheaper in 2025? Not really. While many providers advertise short-term promo deals, the regular monthly price of most Internet plans has continued to increase. AutoPay requirements, term agreements, and post-promo price jumps all contribute to higher long-term costs.

Do smaller ISPs offer cheaper service? They offer better long-term value rather than deep discounts. Independent ISPs pay wholesale access fees that make up most of the monthly cost, so their advantage comes from transparent pricing, no contracts, and more predictable bills, not massive introductory discounts.

Does switching to an independent ISP affect my TV or IPTV options? No. Independent ISPs use the same backbone networks as major carriers, so IPTV apps, live TV services, and streaming platforms work normally. The main difference is usually clearer billing and fewer bundle-related restrictions.

Which provinces have the best Internet prices? Typically Ontario and Alberta, where multiple cable and fiber options overlap. Atlantic Canada and rural regions face higher average rates due to limited infrastructure.